Headlines have been dominated recently by bitcoin's drop in value, but this hides the activity that continues to happen around bitcoin and blockchain technology in general.

In particular, four startup ventures tell a very interesting story and reflect the general level of activity in this space.

Quantave aims to provide intra-exchange connectivity and liquidity for digital currencies, as well as connect traditional financial institutions to digital liquidity pools.

XBTerminal is a point-of-sale solution to make it easy for merchants to offer digital currencies payments, even for offline transactions.

PayWithBolt aims to provide an online service that make it easier for websites to accept payment in any digital currency.

Kryptonomic is aiming to provide a clearing network for (financial) derivatives, using smart contracts.

All four companies presented at a recent Nesta-sponsored event in London, celebrating the rise of digital currencies.

While bitcoin (with the most advanced supporting infrastructure) is the primary target for most of these services, all are architected on the basis that there will be other digital currencies, and that they will all require similar services.

In essence, firms like these are building the plumbing for a new payments/money infrastructure that fundamentally changes the role that traditional financial institutions play. In particular, it acknowledges almost all financial transactions today are digital transactions - i.e., a digital record of a promise from a Payer to pay a Payee a certain amount of money. Some of those records are tied to physical evidence (such as a cheque, deposit receipt, signature or physical machine PIN verification) but a large number are not. Hybrid systems like Apple Pay entrust the 'physical' aspect to a digital device (i.e., the phone and capturing a fingerprint or PIN on that device).

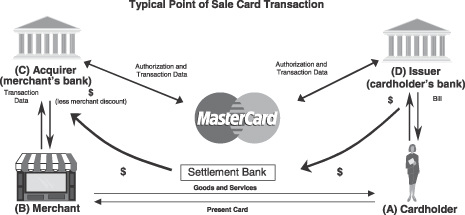

So the leap to an all-digital payments infrastructure is, relatively speaking, not a big one, although it does eventually mean replacing large amounts of 'traditional' technology and infrastructure which collectively provide the guarantees and assurances that payment obligations are correctly recorded and met, as indicated in the diagram below (based on information from MasterCard for a simple single-currency transaction):

Other intermediaries can be involved in this process too - for example, intermediaries that take on currency exchange risk that neither the merchant nor the payer wish to take on, and that the banks may charge too much for.

Digital payments basically allow the payer (or 'cardholder') and payee ('merchant') to exchange value directly with each other, to their respective digital wallets, without any intermediaries. In other words, it works just like cash, but with all the benefits of not having to deal with physical cash.

Will all the intermediaries then disappear? No - but their roles will change, and the whole payments process will get vastly more efficient and cheaper, and enable a lot more people to join in the digital/knowledge economy.

Specifically, banks will (eventually) not be the gatekeepers of payment transactions: instead, they will have a key role in guaranteeing the security of people and business's digital wallets and digital identities. As such, banks will likely have a key role in the new digital payments infrastructure - but it is rather like going back to basics for banks.

What do banks stand for (at least pre 2008)? People associated banks with trust, security, service and (in days gone by) empathy. Banks are trying to rediscover these values and adapt, but it will take time.

But these are key value propositions banks can add, even more so in the digital age. But banks will not need to be involved in every transaction that happens - unless the payers and payees want them to be for reasons of service, etc.

With respect to 'security', banks need to invest heavily in becoming digital security experts: even more than cloud companies, they need to be by far the experts in the field, in order for people to entrust them with their digital wallets. Part of that is under-writing security risk: if wallets get stolen, banks will be on the hook. Today, if digital wallets get stolen, you have very little legal recourse.

Today, with all the innovation happening, there is still a big gap in who will provide those foundational services of managing digital wallets and identities - both key to a stable financial infrastructure and protecting civil interests against criminal activity. I believe the sooner banks and regulators recognise the huge opportunity here and start building up the capabilities they need to carry out these responsibilities, the better for everyone.

But in the meantime, we can expect continued innovation in the basic infrastructure and plumbing underpinning digital currencies, albeit in a high-risk/high-return environment.

RSS Feed

RSS Feed